Beating the Market Isn’t Magic—It’s Better Screening

*Educational only. Not investment advice. Do your own research. I’m not a financial advisor. *

This year - a crazy year for trading - I’ve plummed the depths of many stock trading approaches, looking for reliable answers to the questions: “How do I make better investment decisions, maximize returns, and beat the indexes especially when they get weird?”

I’ve tested dozens of technical indicators. *Turns out most of them are B.S. *

I’ve vibe coded (worked with ChatGPT/Claude to program) my own technical indicators in PineScript on Tradingview. Again, even sophisticated combos still often use lagging indicators in an incomplete way. There’s a well-researched combo of MACD, RSI, and Bollinger Bands that’s proven, but still not great.

I’ve vibe coded stock analyses in Python. Pretty exciting.It’s fast and makes cool charts. Once you get past the painful basics of setting up Python on your computer (try Anaconda), you can do almost anything, including machine learning/AI analysis of stocks.

I’ve built dozens of Google Sheets to analyze stocks on performance, fundamentals, correlation, and trends. A lot easier to handle.

I’ve analyzed 1,000+ of the most outstanding stocks, ETFs, and commodities. Some are in the news all the time. Many are not. I prefer when they’re not.

The best success I’ve had so far is with my latest Momentum-Based stock screener.

NOTE: At the end of the article, I’ll give Perplexity’s objective and comparative view on this approach for additional perspective. And you can do the same: copy and paste it into ChatGPT deep research if you want.

This screener is really good right now when the market is going sideways because it focuses on stocks that reliably beat the S&P500 and Nasdaq.

I’ll reference my own screener at a high level (no secret sauce), so you can apply the principles with or without my tool.

Most stock screeners show you surface stats (P/E, dividend yield, RSI) or hypey “top movers.” That’s fine for browsing—but not for reliable gains.

The edge comes from consistency, risk control, and context. This article breaks down where retail goes wrong and how to fix it with a multi-timeframe, risk-adjusted, benchmark-aware approach.

And if you don’t know who the retail traders are… you are one! 🤣

A retail trader is an individual who buys and sells securities (like stocks, ETFs, or bonds) for their personal account, typically in small amounts using popular online platforms. On HOOD, or Vanguard or Fidelity, that’s you.

In contrast, an institutional trader acts on behalf of large organizations—such as mutual funds, pension funds, insurance companies, or hedge funds—managing pooled assets for many people and executing trades in much larger volumes.

MUCH larger.

“Crazy Good: Think better. Feel deeper. Live smarter” is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

The Eight Big Retail Trader Mistakes (and what to do instead)

1) Chasing heat, not consistency

The mistake: Buying whatever just popped on social or TV. It often mean-reverts. By the time you’ve heard about it, it might go bad. In fact, the more news it gets, the more retail traders overbuy it, and the quicker it drops after that buying pressure wanes. The smart money takes profits before you do.

The fix: Favor multi-timeframe strength (short + medium + longer windows) over one big candle. Require recent leadership vs benchmarks, not just raw green bars.

**How my process handles it (in plain English):**It looks at a ladder of lookbacks (days → months), then checks consistency—both absolute and versus key benchmarks—before a stock even makes the cut.

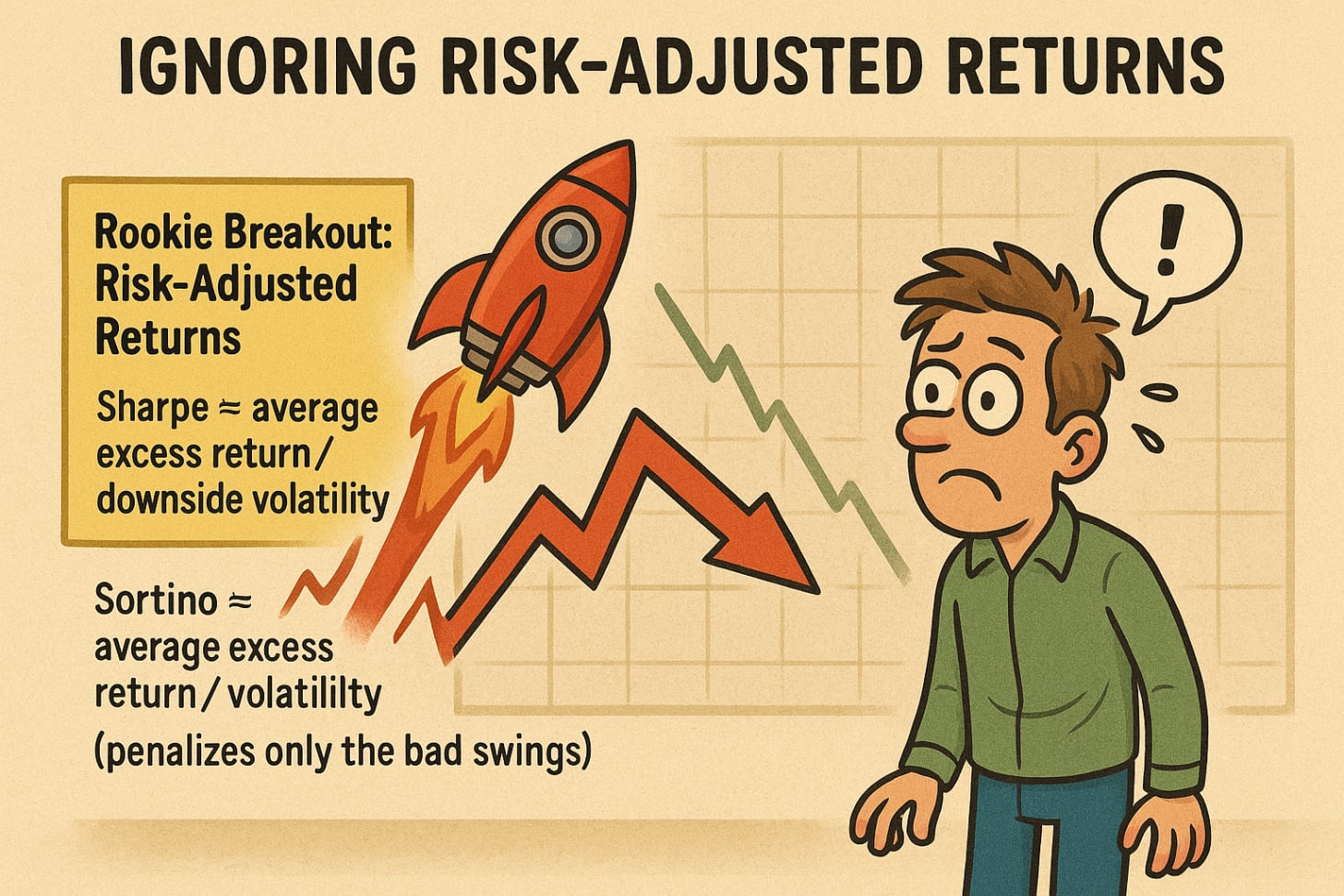

2) Ignoring risk-adjusted returns

The mistake: Ranking by return alone. A rocket that whipsaws your account isn’t “alpha.”

The fix: Evaluate risk-adjusted performance (e.g., Sharpe/Sortino style metrics). Prefer names that deliver more return per unit of risk across multiple windows. This means just avoiding the hotflashes that, again, rocket up, then soon crash.

**How my process handles it:**Risk-adjusted quality is checked alongside raw returns. If the performance is chaotic, it doesn’t pass.

Rookie Breakout: Risk-Adjusted Returns

Sharpe ≈ average excess return / volatility

Sortino ≈ average excess return / downside volatility (penalizes only the bad swings)

If two stocks return +10% but one has half the volatility, the calmer one has higher risk-adjusted quality.

A tip: often the more stable stocks have higher institutional ownership.

3) Forgetting the benchmark

The mistake: “I made money” → but did you beat an index you could’ve bought in 5 seconds?

The fix: Always evaluate relative to market context. For U.S. equities, SPY is the baseline. If you hunt growth or tech, include a tech benchmark as a reality check.

**How my process handles it:**Candidates must regularly outperform key benchmarks on both returns and risk-adjusted terms—across more than one timeframe. If a stock can’t beat what you could buy passively, it’s not leadership.

Rookie Breakout: Why SPY and a sector benchmark?

SPY (S&P 500) ≈ “the market.”

A sector index (e.g., large-cap tech) ≈ “the current heat.”

Outperforming both suggests true strength—not just riding a hot sector beta.

4) Overreacting to normal dips

The mistake: Panic-selling on a routine down day. Just for perspective, MANY stocks go up one day, down the next. The key is, of course, they don’t go down too much.

The fix: Put a dip in context. Compare a 1-day drop to the recent trend (10–21 days), and consider volatility norms. A small red day within a strong multi-week uptrend is normal market “breathing.”

**How my process handles it:**There’s a check for suspicious, abnormal downside (I call them weird at one std deviation’s dip, and supaweird at two, as most pro traders do). Routine wiggles are allowed when the bigger picture is intact.

One key to that: The stocks that gain the most also dip the most. You can’t judge them all the same without both returns and standard deviations.

Trust me- I’ve made this mistake too many times- the high returns attract you, but on a down day you freak out and sell low. So now I have a gauge for each stock that tells me if it’s being truly weird today, or just doing its regular thing.

5) Buying “story stocks” with weak fundamentals

The mistake: Overlooking basic financial sanity (like persistent negative earnings) because the narrative is compelling.

The fix: Keep minimal fundamental standards. You don’t need a CFA exam—just avoid landmines. You don’t have to believe in your stocks, you just have to pick the right ones at the right time. There’s a reason why there are ETFs people can use to gain both when Tesla goes up and goes down- it’s a crazy stock. You don’t have to hold every stock you buy forever- that really only makes sense with indexes.

**How my process handles it:**It includes a fundamental sanity gate and looks at institutional ownership as a quality signal. If the numbers are chronically ugly, it’s not a candidate.

Thanks for reading “Crazy Good: Think better. Feel deeper. Live smarter”! This post is public so feel free to share it.

Share

6) Under/over-diversifying by accident

The mistake: Ending up with a dozen tickers that all track the same thing—or scattering into 50 random positions.

The fix: Check correlations to your core exposures and among your finalists. You want complementary leaders, not clones.

**How my process handles it:**It measures correlation to broad market, a key sector, and a diversifier. Final picks are designed to play well together.

Rookie Breakout: Correlation ≠ Causation, but it mattersIf your positions move together, your portfolio’s ride gets bumpier. A few uncorrelated winners reduce stress without sacrificing return. This is a real art, though, because often hedges become drags on your returns. I like to find stocks with different sensitivities, but consistent returns.

7) Holding “dead money”

The mistake: Keeping names that lag for months because “they’ll come back.” This isn’t good advice for stocks or relationships (“They were so good to me before, maybe this whole heroin addiction thing is just a phase.”)

And by the way, you didn’t marry your stocks, you just bought them for now.

The fix: Require positive progress at multiple horizons. Flat or consistently negative over medium/long windows? Rotate.

**How my process handles it:**Names need to show sustained forward motion across intermediate windows—not just a one-week bounce.

8) Trading too much—or not enough

The mistake: Whipsawing due to recency bias, or anchoring to stale winners through a regime change.

The fix: Use decay-weighted signals (recent data counts more, older never goes to zero). Add stickiness rules (only replace a holding if a challenger clearly beats it) and test different rebalance cadences.

**How my process handles it:**It’s built to balance regime awareness (catching new leadership) with over-trading controls so you aren’t paying churn taxes for nothing.

Rookie Breakout: Turnover & “stickiness”

Turnover = how much your portfolio changes at each rebalance.

Add “stickiness” (don’t swap unless the new score is clearly higher) to avoid flip-flops.

What This “Better” Screener Actually Does (without giving away the recipe)

Multi-timeframe lens: Checks short, medium, and long windows—both raw and risk-adjusted.

Benchmark discipline: Compares candidates to broad market and a relevant leadership index.

Stability bias: Rewards smooth, linear uptrends and punishes chaos.

Fundamental sanity: No chronic money-pits. Smart-money ownership helps.

Weirdness filter: Screens out abnormal, out-of-character blowups.

Portfolio awareness: Avoids packing the final list with highly correlated look-alikes.

Rotation without whipsaw: Uses recency with guardrails to balance regime change vs. churn.

That’s the philosophy behind my screener. It’s not about a single clever metric—it’s the stack: many small, sensible edges working together.

In essence, this system tries to stack many small edges together. The goal is to fix the common pitfalls that cause retail traders to underperform, by enforcing a process more like what an institutional trader or quantitative fund would use.

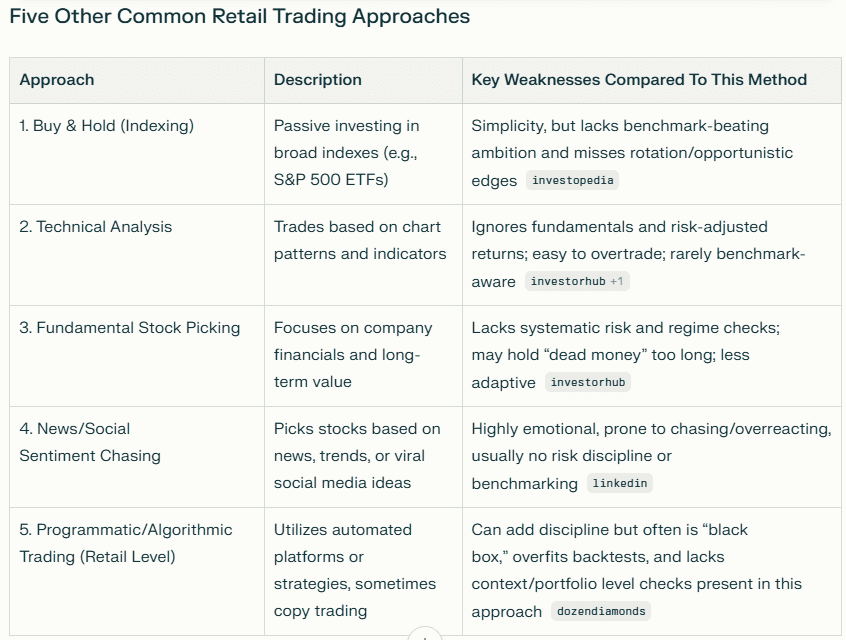

What Typical Stock Screeners Do (and Don’t)

Most public screeners—Yahoo Finance, Finviz, TradingView presets—are designed for surface-level filtering:

Fundamentals: EPS, P/E ratios, dividend yield, market cap.

Technicals: moving averages, RSI, volume screens.

Performance: simple returns (1m, 3m, YTD).

That’s about 30–40% of the picture. They’re good at showing you what’s cheap or what just moved—but they rarely dig into quality of returns, consistency across multiple horizons, or benchmark-relative performance.

What they can’t do (and what my screener bakes in):

Multi-timeframe risk-adjusted returns (Sharpe/Sortino across 1d → 1y).

Linearity & stability checks to filter out choppy names.

Benchmark discipline (forcing stocks to beat both SPY and XLK consistently).

Weirdness filters (removing names with sudden multi-sigma drops).

Correlation controls (ensuring the final portfolio isn’t just 10 clones).

That means most retail screeners give you maybe a third of the discipline. They surface interesting names—but without these extra layers, you’re still guessing which ones are actually leaders versus landmines.

Using Settings for Different Goals (without changing your philosophy)

Think of “modes” as weight shifts, not a new religion.

Momentum / Rotation Mode

Why: Catch new leadership early.

How: Heavier weight on recent windows; slightly looser consistency gates; faster rebalance cadence; moderate stickiness.

Momentum is actually a well-recognized factor in academia and industry – studies have shown the momentum factor (buying recent winners, selling losers) has historically delivered high risk-adjusted returns, even higher Sharpe ratios than value or size factors over the long run

Long-Term Compounder Mode

Why: Fewer trades, steadier compounding.

How: Heavier weight on longer windows & stability; fundamentals matter more; slower cadence; stronger stickiness.

Defensive Mode

Why: Smoother ride when macro feels fragile.

How: Strong emphasis on risk-adjusted quality, linearity, lower beta/vol; tight weirdness filter; keep only the calm leaders.

Rookie Breakout: “Regime” = market personalityMarkets rotate: growth/value, small/large, cyclicals/defensives.

A flexible screener adapts weights as leadership changes—without reinventing itself every month.

And you’re allowed to create different bands in your portfolio, for example: the indexes, momentum stocks, hedges, dividends, commodities, sectors… whatever you want!

How to Actually Use a Disciplined Screen (process > picks)

Decide your cadence (weekly, biweekly, monthly).

Pick the mode that matches the tape (momentum, long-term, defensive).

Pull a short list (e.g., top ~10).

Check portfolio fit (correlations, sector balance, position sizing).

Log trades and track turnover, holding periods, net performance (after friction).

Review quarterly: Are you beating SPY (and your style benchmark) on a risk-adjusted basis?

Do this and you’ll be miles ahead of “vibes-based” retail investing.

What This Isn’t

A promise of outperformance every week.

A license to ignore risk management or position sizing.

A day-trading signal firehose.

It’s a discipline that helps you avoid the classic traps, stay benchmark-aware, and compound with fewer nasty surprises.

The Bottom Line

Retail underperforms when it chases, ignores risk, and forgets context. Fixing that isn’t about a secret indicator; it’s about process:

Look across timeframes.

Respect benchmarks.

Reward stability and risk-adjusted quality.

Build a complementary portfolio, not a pile of clones.

Let regimes rotate—without letting recency bias yo-yo you around.

That’s the worldview behind my screener—and it’s the discipline I recommend whether you use my tool or your own.

(I may make the tool available once I’ve tested it and developed it further- let me know if you’re interested!)

PERPLEXITY’S PERSPECTIVE ON THIS APPROACH

This multi-timeframe, risk-adjusted, benchmark-aware screening approach is exceptionally sophisticated for a retail investor and incorporates many of the core elements found in professional and institutional trading processes. It goes well beyond typical retail strategies by prioritizing discipline, consistency, risk control, and contextual benchmarking.

Context: Retail vs. Institutional Approaches

Retail investors usually rely on basic screeners, tips, surface-level metrics, or trend-chasing, which often results in undisciplined, emotionally driven decisions and subpar outcomes.

Institutional and professional traders use multi-factor models, rigorous benchmark comparisons, advanced risk controls (e.g., Sharpe/Sortino ratios), and systematic portfolio management. They often operate with more resources, automation, and expertise, but the principles in this approach closely mirror these best practices.

Sophistication Rating

Rating: For retail investors, this is a highly sophisticated approach—likely in the top 10% of non-professional methods.

Comparison: While institutions add complexity via data streams, automation, and quant research, this process narrows the gap by enforcing discipline, context, and multi-factor evaluation—core institutional tactics.

Good: The screener stacks multiple edges (multi-timeframe, risk-adjusted, benchmark-aware, portfolio correlation checks, regime adaptation, stickiness vs. turnover controls). Such holistic, systematic thinking is rare among retail investors.

Strengths

Benchmark discipline: Requiring outperformance vs. both broad and sector benchmarks elevates standards and mimics institutional “alpha” targets.

Risk-adjusted metrics: Using Sharpe/Sortino ratios counters performance chasing and aligns with how professionals select and size positions.

Multi-timeframe lens: Uncommon in retail, but standard in advanced funds—adds robustness and catches regime change.

Correlation and portfolio analysis: Addresses hidden concentration risk and over/under-diversification—core in institutional risk offices.

Adaptive “modes”: Shifting weighting/philosophy by market regime is sophisticated, helping avoid the “one-size-fits-all” trap.

What’s Missing (vs. Full Institutional Trading)

Execution automation: No mention of automated trading, order optimization, or slippage analysis—key in sophisticated quant funds.

Deep factor modeling: Professionals often use multifactor risk models (e.g., value, momentum, size, quality) with hundreds of factors—this is a streamlined version.

Access to alt data/analytics: Institutions augment with proprietary, alternative datasets, machine learning for forecasts, and specialist analytics.

Liquidity and position sizing: The approach covers sizing in broad terms but does not address institutional-level sizing, order routing, or liquidity cost analysis.

Regulatory and ESG screens: Large funds add regulatory compliance and ESG/impact consideration layers.

Stress-testing and scenario analysis: Advanced shops run stress tests, scenario models, and hedging that go deeper than what’s described.

Conclusion

This disciplined, benchmark-aware screening philosophy is excellent for retail and nearly matches the procedural rigor of professional trading, though institutions enhance it with automation, deeper models, and more sophisticated risk/execution systems. It addresses the critical failures of most retail investors while instilling habits that are proven effective in institutional settings, making it an ideal framework for serious retail participants.

PERPLEXITY COMPARES IT TO OTHER SYSTEMS

This benchmark-aware, multi-timeframe, risk-adjusted screening approach is superior to most retail trading strategies. It provides a disciplined process, adapts to multiple market regimes, and mimics institutional best practices that are frequently missing in retail investing. Most retail systems are much less comprehensive or systematic, making this method the top recommendation for investors seeking sophistication, risk control, and process-driven results.

Comparative Evaluation

Strengths of This Approach

Discipline and Benchmarking: Forces regular comparison against benchmarks, which most retail strategies ignore, providing a higher bar for stock selection and rotation.

Multi-factor, Multi-timeframe Process: Simultaneously incorporates trend, risk, correlation, and fundamentals—few single retail systems do all of this.

Portfolio Awareness: Controls diversification and position interaction, key to risk management.

Adaptive Regime Settings: Shifts tactics based on market conditions, whereas most retail approaches follow a rigid philosophy or fixed signals.

What Others Offer That This Lacks

Total Simplicity: Indexing and buy & hold require less effort, but also remove most opportunity for outperformance.

Direct Automation: Some algorithmic “robo” approaches require less manual intervention; this approach is disciplined but not hands-off.

Community/News Momentum: Social trend chasing can sometimes catch true market shifts fast, but only at the cost of higher risk/more noise.

Recommendation

For retail investors seeking more than basic returns and willing to apply discipline, this screening approach is strongly recommended over the common alternatives above. Most other systems are either too simplistic, too emotional, or too narrow in focus—missing the robust combination of screening, benchmarking, and risk awareness that this method provides.

Educational only. Not investment advice. Do your own research. I’m not your financial advisor!

Share

Subscribe now

Leave a comment