The Crazy Good Dividend Investing Guide

A quick note for readers and subscribers: The Complete Guides and Transformation Tools I’m building will eventually be paid-only. My regular articles will remain free. This is a sample of what I’m building toward in the paid realm, and it’s free for now, so enjoy!

Subscribe now

My good substack friend - aka internet acquaintance I’ve never met but we’ve messaged a bunch? and a great creator you should follow as well? yes! - Dennis Gorbunov, has been posting about dividend equities recently, and coincidentally, I’ve been working on this guide.

Dividends are certainly a factor in my stock picking, and I think you’ll see why once you get through this comprehensive guide!

Why Dividend Investing Fits a Crazy Good Life

While most of the investing world chases hype, volatility, and quick wins, there’s a quieter path—one built on consistency, trust, and companies that literally pay you to hold steady.

Dividend investing is more than a financial strategy. It’s a way of aligning your money with your mindset. It lets you stop chasing and start building.

It matches the Crazy Good philosophy: Grow from the inside out. Build wealth that reflects who you are—not who you’re trying to impress.

This guide is for people who think fast, feel deep, and want their money to reflect both their vision and their values.

We’ll cover:

Why dividends matter in any market

How to evaluate great dividend companies

What mistakes to avoid (and how to sleep better at night)

How to structure a portfolio that supports your future and your nervous system

Because your portfolio isn’t just a pile of numbers—it’s a mirror of your beliefs about time, trust, and what a “good life” really looks like.

**🧠 HEAD CHECK:**What if your money could reflect your values instead of your fears?

What Makes Dividend Investing Different

When you buy dividend-paying stocks, you’re not just buying the hope of a price increase—you’re buying into companies that generate consistent profits and share them with you.

That creates three layers of value:

Emotional stability: You get paid even in market downturns.

Financial durability: Dividends compound over time, especially when reinvested.

Strategic clarity: You can evaluate companies on fundamentals, not hype.

The best dividend stocks are usually led by long-term thinkers, not hype chasers. They don’t need to make headlines—they just quietly make money.

**💓 HEART CHECK:**What would change if your wealth was built on trust, not adrenaline?

Types of Dividend Stocks (and Why They Matter)

Not all dividend stocks are created equal. Here’s a breakdown of three key categories and why they belong—or don’t—in your portfolio:

🏛️ Dividend Kings and Aristocrats

These companies have raised dividends for 25+ (Aristocrats) or 50+ (Kings) consecutive years. They’ve survived recessions, wars, pandemics, and still prioritized shareholders. They’re the tortoises in a market full of hares.

Coca-Cola

Procter & Gamble

Johnson & Johnson

Emerson Electric

These aren’t “explosive” stocks. They’re the ones you can count on when the world wobbles.

🚀 Dividend Growth Stocks

Lower yield, higher upside. Think Microsoft, Apple, or Broadcom—companies that may yield 0.5–1.5%, but grow those payouts aggressively over time. These stocks often sit at the intersection of innovation and stability.

💰 High Yielders (With Caveats)

Energy, telecom, and REITs often pay 5–8%+ yields. That sounds great… unless those dividends aren’t sustainable. Before buying a high-yielder, check their debt, cash flow, and payout ratios.

**🧭 GUT CHECK:**Are you choosing stocks that calm you down—or ones that light you up too fast?

What You’re Really Buying

A dividend stock isn’t just a company—it’s a relationship. You’re not just betting on upside; you’re betting on consistency, values, and leadership.

Done right, this strategy compounds not only wealth, but peace of mind.

But only if you take it seriously. Only if you check your ego, and your FOMO, and choose systems that are smarter than your mood swings.

**🔄 LIFE CHANGE CHECK:**What would happen if your money stopped chasing heat and started building warmth?

How Dividend Stocks Build Wealth Over Time

Dividends aren’t just a nice bonus. They’ve historically accounted for 30–40% of total market returns.

From 1930 to today, reinvested dividends have made the difference between average investors and wealthy ones.

But it’s not just the math—it’s the mindset.

Dividend investing encourages:

Long-term thinking

Patience

Reduced emotional trading

Reliable income through recessions and inflation

It also makes investing feel tangible. You’re not just watching a green number go up. You’re getting paid—in real money—for staying invested.

**🧠 HEAD CHECK:**When you look at your portfolio, how much of it is designed to reward holding, not just hoping?

Dividend Growth vs. High Yield: Picking the Right Fit

People often chase the highest yield they can find… and regret it later.

A stock paying 7–8% might look great—until it cuts its dividend, tanks in price, or turns out to be masking deeper business problems.

On the other hand, dividend growth stocks like Microsoft or ADP might yield 1–2% today but increase their payouts 10% annually, turning modest yields into powerful long-term income.

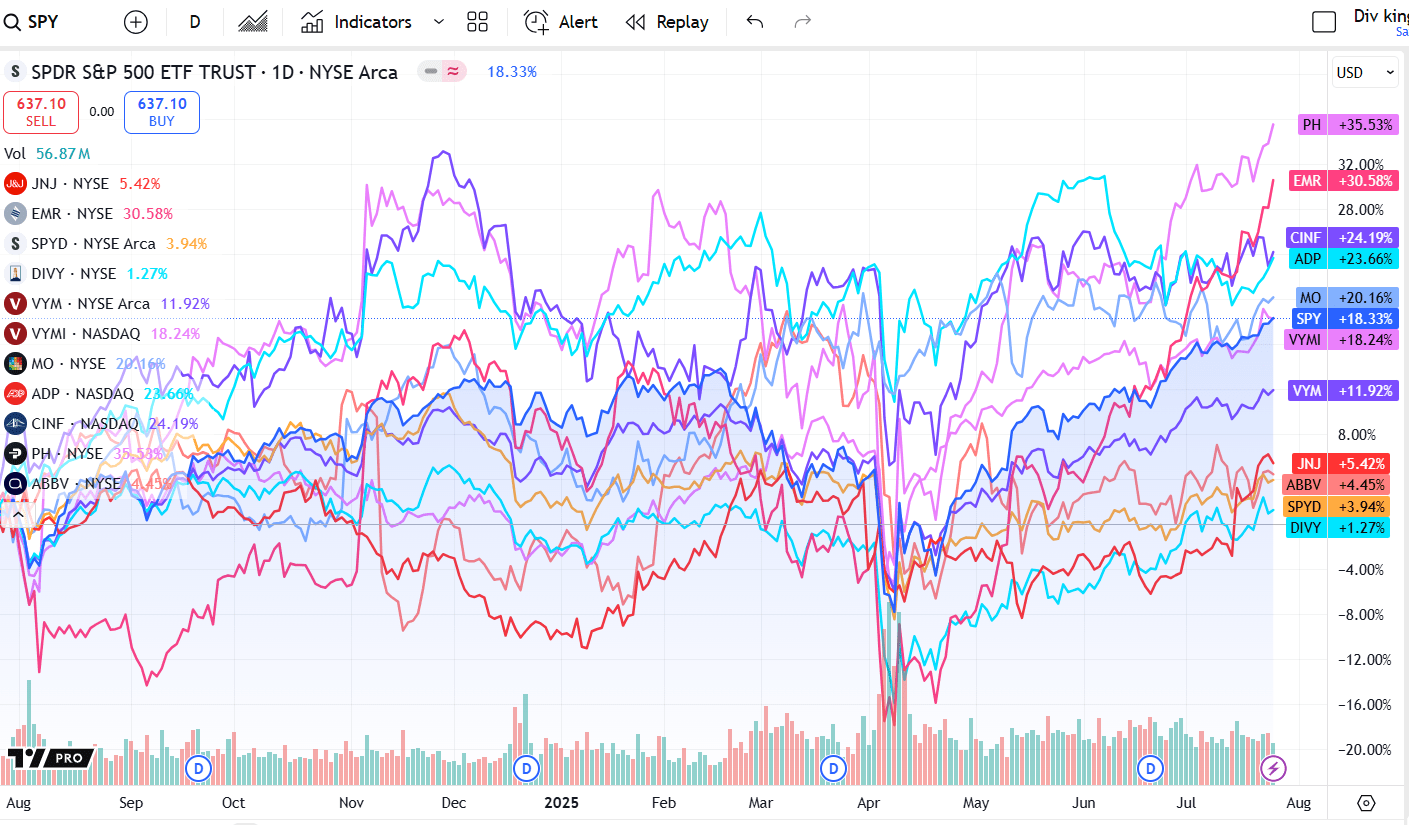

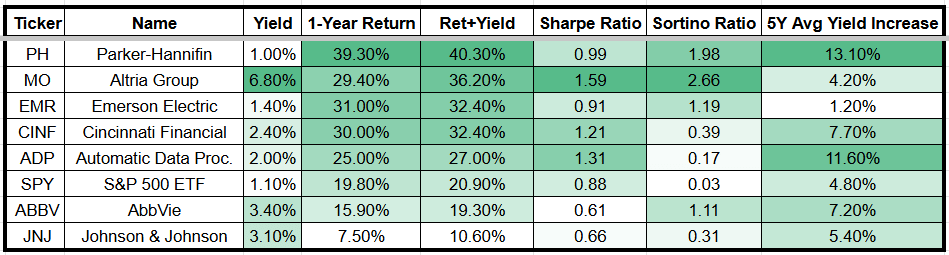

This shows some of the highest returns among dividend kings, but not the yields. Ideally, you want to look at both, and more!

There’s no “best” option. The real question is what you value:

Immediate income?

Long-term compounding?

A mix of both?

Some other things to consider!

**💓 HEART CHECK:**Are you drawn to high yield because it fits your goals… or because it soothes your short-term anxiety?

Building a Dividend Portfolio That Matches Your Life

Your investing strategy should match your real life—not just your risk tolerance on paper.

In your 30s, you might prioritize dividend growth and compounding. In your 60s, you might favor higher income and lower volatility.

But it’s not just about age—it’s about attention span, stress tolerance, and time.

Here’s one model to consider with some examples:

20s–30s: Dividend growth (Microsoft, Apple, Broadcom)

40s–50s: Blend of growth + stable income (Pepsi, ADP, Realty Income)

60s+: Reliable yield and payout history (Johnson & Johnson, utilities, REITs)

You’re not building a portfolio. You’re building a system that supports your future self.

**🧭 GUT CHECK:**If you didn’t check your portfolio for 6 months, would you feel calm about your current holdings?

Who do you know that needs to read this? This post is public so feel free to share it!

Share

The Risks No One Talks About

Every investment has risk. But some risks don’t show up in charts.

Yield traps: Stocks that look generous but are financially shaky

Overconcentration: Too many utilities or REITs in one portfolio

Complacency: Relying on past performance without rechecking fundamentals

False security: Confusing “safe” brands with solid financials

And then there’s the biggest one: emotional risk.

Making rash decisions when a dividend gets cut, or selling a great stock during a downturn.

The solution isn’t perfect prediction. It’s structural clarity and regular review.

You don’t need to know the future—you just need a system that adapts when it changes.

**🔄 LIFE CHANGE CHECK:**Where in your finances have you been on autopilot… and is that helping or hurting you now?

🛠️ Building a Dividend Portfolio That Matches Your Life

Most investing advice doesn’t take real human life into account.

It assumes you’re a spreadsheet with a risk tolerance score, not a person with shifting goals, changing energy levels, family dynamics, and evolving ideas of what “enough” looks like.

A Crazy Good approach to dividend investing asks a different question:How can your portfolio adapt as you grow?

Here’s a simplified framework based on life stage—not just age, but where you are mentally, emotionally, and financially:

In Your 20s and 30s: Growth Over Comfort

Prioritize dividend growth stocks like Microsoft, Broadcom, or Visa.

You probably don’t need the income now—so focus on companies that raise payouts every year.

Use tax-advantaged accounts like Roth IRAs and reinvest everything.

In Your 40s and 50s: Blend and Balance

Introduce stable, moderate yielders (2–4%) to generate cash while compounding.

Include some REITs or utilities—but avoid overloading on low-growth names.

Use dividend income to rebalance your portfolio, not just spend it.

In Your 60s and Beyond: Reliability and Resilience

Emphasize sustainability over speculation.

Dividend Kings (50+ years of increases) and low-volatility ETFs become your foundation.

Cash flow becomes more important than price appreciation—but don’t completely ignore growth.

You’re not “aging into caution”—you’re learning to optimize for peace of mind, not just percentage points.

**🧠 HEAD CHECK:**Are you investing according to your current goals and life rhythms—or still using a strategy from a past version of yourself?

🧬 The Psychology of Dividend Investing: Emotional Strength > Market Genius

Dividend investing looks “boring” to adrenaline-chasing traders. But in reality, it requires emotional strength most people don’t cultivate.

You have to:

Stick with a system even when the market is throwing a tantrum.

Avoid chasing the highest yields when they’re too good to be true.

Trust long-term compound growth instead of reacting to headlines.

This isn’t about outsmarting Wall Street. It’s about outlasting your own anxiety.

Dividend investing gives you structure—automatic rewards, consistent signals, and concrete reminders that you’re still on track, even when the market gets weird.

But that’s only true if you actually stay the course.

**💓 HEART CHECK:**When your account balance is down, what helps you feel grounded again—numbers or narratives?

🧠 How to Avoid Yield Traps Without Getting Cynical

High dividend yields can seduce even smart investors.

The logic is simple: “Why wouldn’t I want a 7% yield when everything else is paying 2%?”

Because sometimes that yield is an illusion.

Common red flags:

Payout ratio above 90% (or over 100%, which means the company is borrowing to pay you)

Shrinking revenue or cash flow

Sector-wide stress (e.g., real estate or telecom meltdowns)

Sudden spikes in yield from price drops

And yet, not all high yields are traps. Some come from temporary market mispricing, or industries investors have unfairly punished.

Here’s the nuanced play:

Instead of asking “how high is the yield?”, ask:

What’s the business model?

Can they actually afford this payout?

Have they raised it consistently in good and bad years?

You don’t need to be paranoid. You just need a filter.

**🧭 GUT CHECK:**When a yield looks amazing… is your excitement based on analysis, or just emotional relief?

Is this article good? Crazy Good is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

Share

🔁 How to Reinvent Your Strategy Without Starting Over

One reason people stick with broken investing habits? They don’t want to start from scratch.

The good news: you don’t have to.

The Crazy Good approach is about adaptive iteration.

You take what’s working, refine what’s not, and build systems that reflect who you’re becoming—not just who you were when you started.

Start with a few stable, proven dividend stocks. Add thematic exposure as you grow. Use income to fund future investments, not just plug short-term gaps.

And when you mess up? Learn. Adjust. Keep going.

This isn’t about perfection—it’s about forward motion with your eyes open.

**🔄 LIFE CHANGE CHECK:**If you gave yourself permission to update your strategy, not abandon it—what would change?

🧪 Real-World Dividend Profiles: What Great Actually Looks Like

Rather than theorizing, let’s break down a few real companies that show how this plays out across different dividend investing styles.

These are not stock picks. They’re living examples of different dividend profiles—and how they support different goals.

🟢 Microsoft (MSFT): Quiet Compounding Royalty

Yield: ~0.8%

Dividend growth: +10–15% per year

Payout ratio: 25–30%

Moat: Dominates business software, strong AI positioning

Fit: Ideal for long-term dividend growth, not short-term income

Microsoft’s dividend doesn’t scream, it whispers. But in 5–10 years, it grows into a roar.

🟨 Realty Income (O): Monthly Paycheck Machine

Yield: ~5.5%

Dividend growth: 2–4% annually

Payout ratio: High, but normal for REITs

Moat: Retail and commercial real estate with long leases

Fit: Monthly income you can set your life to

This is the utility belt of dividend portfolios: steady, boring, essential.

🟥 Altria (MO): High-Yield Controversy with Cash Flow

Yield: 8–9%

Dividend growth: Low to moderate

Payout ratio: ~80%

Moat: Pricing power, brand loyalty, but declining product category

Fit: Contrarian income play for experienced investors

Altria pays you now—but you’ll want to keep an eye on the long-term thesis. This isn’t one to forget in a drawer.

**🧠 HEAD CHECK:**Which of these profiles most closely matches your goals—and which are you drawn to for the wrong reasons?

🧱 How to Build a “Crazy Good” Dividend Portfolio

Let’s say you’re starting fresh. Here’s a flexible blueprint that balances yield, growth, and peace of mind across market cycles.

The Core (60–70%)

These are your dividend growth and blue-chip holdings—reliable, steady growers that anchor your portfolio.

Examples: Microsoft, J&J, ADP, Costco, Pepsi, Broadcom, SCHD (ETF)

The Income Layer (20–30%)

These are your higher yielders and REITs. They provide current income and diversification.

Examples: Realty Income, NextEra Energy, VICI, EPD, JEPI (ETF)

The Thematic or Strategic Layer (5–15%)

This is your experimental sandbox: emerging markets, tech dividends, or under-the-radar ideas.

Examples: Taiwan Semi, URA (nuclear ETF), GDX (gold miners), bank preferreds, covered-call ETFs

Additions can rotate quarterly or annually depending on performance, thesis durability, and macro trends.

**❤️ HEART CHECK:**When you imagine getting quarterly (or monthly) checks from your portfolio, how does that feel—steady, calming, motivating… or stressful?

💡 When to Buy (and How to Think About Timing)

Dividend investing is long-term by design—but that doesn’t mean timing never matters.

If your favorite Dividend Aristocrat is:

Trading 20% below its historical valuation

Still growing cash flow and earnings

Increasing its dividend while others are cutting

…you may want to lean in.

That’s not “timing” in the trading sense. It’s paying attention to cycles and buying when others are nervous.

You don’t need to catch bottoms. You just need to buy good companies when they’re not being priced like royalty.

Want to dollar-cost average into a position? Great.

Want to make lump-sum purchases during volatility? Also great.

The right time to buy is when the business is strong—even if the stock price isn’t.

**🧭 GUT CHECK:**Do you trust your ability to tell the difference between a short-term drop and a long-term decline?

🧠 Tools and Habits That Keep You on Track

The system matters more than the moment.

If you want to avoid emotional decisions and compound your wins, build these habits:

Quarterly reviews: Don’t check your portfolio daily. Review your holdings every 3 months to adjust based on your strategy, not your mood.

Dividend tracking: Use a tracker like Sharesight, Google Sheets, or a brokerage dashboard to watch your income rise.

Watchlists with guardrails: Maintain a list of stocks or ETFs you’d like to own—but only when certain metrics are met (yield, payout ratio, etc).

Write your reasons: For every buy or sell, write your rationale. Future you will thank you.

**🔄 LIFE CHANGE CHECK:**What’s one habit you could build that would make investing feel less like a gamble and more like a craft?

🌍 Modern Forces Reshaping Dividend Strategy

🧭 The ESG Wave: Meaning, Moats, and Materiality

Environmental, Social, and Governance factors aren’t just a feel-good filter — they often reveal whether a company can thrive in an increasingly complex world.

Companies with strong governance tend to protect shareholder capital and maintain long-term stability.

Firms with sustainability strategies are often better positioned for regulatory and cultural shifts.

Social and workforce policies reflect whether a business is building trust or burning it.

But ESG isn’t one-size-fits-all. Some dividend investors want alignment with their values. Others want long-term moat protection. You can have both—just don’t let the acronym substitute for actual analysis.

**🧠 HEAD CHECK:**Are your dividend investments aligned with the kind of world you want to live in—or just the one you think you’re stuck with?

🤖 The Role of AI and Automation

Technology is changing everything, including the way we build and manage dividend portfolios.

Machine learning can now:

Flag dividend cut risk before humans catch it

Predict dividend growth based on macroeconomic signals

Filter companies with durable pricing power and cash flow quality

That doesn’t mean you should blindly follow a robo-advisor. But it does mean you can use tools (like ChatGPT, Perplexity, or quant filters) to take some of the grunt work off your plate—and free up more time to think clearly.

**💓 HEART CHECK:**If investing felt easier and smarter, would you be more consistent with it?

🧠 Psychological Pitfalls (and How to Dodge Them)

Dividend investing is designed to be boring — and that’s precisely why it’s so hard.

The most dangerous enemies aren’t the market, taxes, or inflation. They’re you.

Here’s what to watch for:

Yield obsession → chasing high numbers without checking the story

Complacency → ignoring a declining business because “they’ve always paid”

Loss aversion → selling quality companies too early to “protect” paper gains

Impatience → forgetting that compounding is boring before it’s amazing

Recency bias → assuming a 5% dip means something’s broken

This is where your system saves you. Or betrays you.

**🧭 GUT CHECK:**What pattern in your investing behavior has cost you the most—emotionally or financially?

🧰 Advanced Tactics for People Who’ve Done the Work

Once you’ve mastered the foundation, here are some strategies that add power to your plan — but only if you’re ready for them.

🧳 International Dividend Exposure

U.S. stocks are great—but 40% of global dividends come from outside America. Add diversity by looking at:

Nestlé, Unilever, Roche (Eurozone)

Canadian banks (higher yield, lower volatility)

ETFs like VYMI or IDV for global coverage

Watch out for foreign tax withholding. Use tax-advantaged accounts when possible.

💸 Cash-secured puts (for the bold)

Want to buy a dividend stock only if it drops to a certain price?You can sell a cash-secured put — get paid now, and potentially own it later at a better price.

Works best on companies you want to hold anyway.

🛡️ Defensive layering (for retirees or cautious investors)

Use “bulletproof” ETFs or dividend-focused funds to create a predictable baseline:

SCHD (U.S. dividend blend)

VIG (dividend achievers)

JEPI or JEPQ (income-focused with options overlays)

Use individual stocks or thematic picks for upside, but anchor with consistency.

**🔄 LIFE CHANGE CHECK:**Which of these advanced tools actually fits your temperament—and which one sounds cool but would stress you out in practice?

🧭 Final Words: Your Wealth, Your Rhythm

Dividend investing isn’t magic. It won’t make you rich overnight.But it will make you smarter, calmer, and more grounded over time.

You don’t have to chase every headline. You don’t have to time the market.You just need to know:

What matters to you

What companies reflect that

And how to build a system that rewards patience, not panic

Crazy Good investing is aligned investing.It’s personal. Purposeful. Sustainable.

And when done right?

It doesn’t just grow your net worth.It expands your peace of mind.

🧠 HEAD CHECK:

Is your current strategy building clarity—or just adding noise?

💓 HEART CHECK:

Which dividend investment actually feels like the kind of life you want to live?

🧭 GUT CHECK:

Do your decisions come from wisdom—or from worry?

🔄 LIFE CHANGE CHECK:

What would change in your life if your money started showing up like the person you’re becoming?