WHY Does Warren Buffet Think United Healthcare Is Worth 1.57 Billion?

Warren Buffet / Berkshire Hathaway just invested 1.57 billion in United Healthcare. Yeah, the company with the assassinated CEO and the government legal troubles.

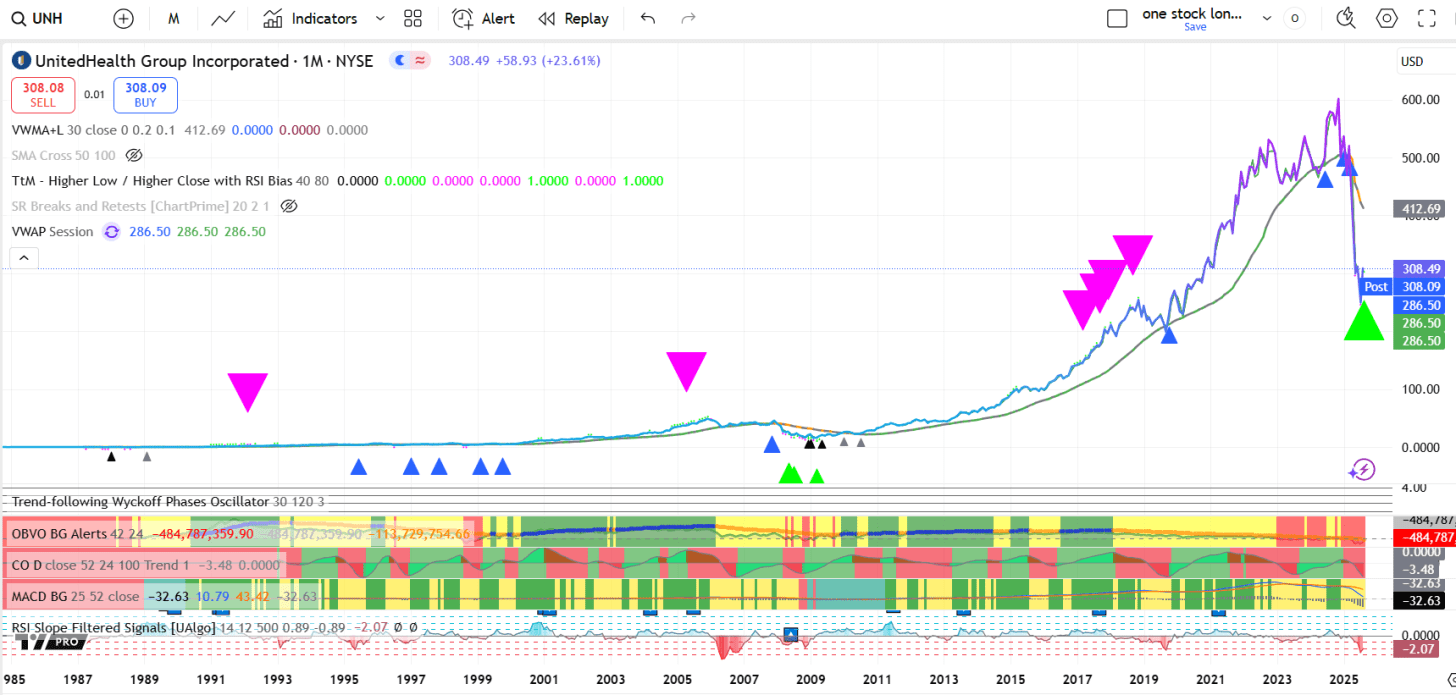

Its stock price was down 57% year-on-year just a couple weeks ago.

Now, it might be one of those buy-the-undervalued-but-fundamentally-good stock play by Berkshire. Buy low, sell high later.

But is it more than that?

Does UNH have a moat against competitors?

How secure an investment would it be for a retail investor like me?

How long would I have to hold it?

What could I expect?

So I ran this CGPT Deep Research query.

Here’s what ChatGPT came up with via its impressive new(ish) Deep Research function:

⚠️ Disclaimer: I am not a financial advisor. The information in this article is for educational and informational purposes only and should not be taken as financial, investment, or trading advice. You should do your own research and consult with a licensed financial professional before making any investment decisions.

UnitedHealth Group (UNH) – Investment Outlook After Recent Setbacks

Recent Challenges and Stock Performance (2024–2025)

UnitedHealth Group’s stock has plunged from an all-time high around $630 in late 2024 to roughly the low $300s by mid-2025 – levels not seen since 2020. This ~50% collapse was driven by a confluence of company-specific setbacks and industry headwinds.

In December 2024, UnitedHealth’s UnitedHealthcare division CEO, Brian Thompson, was tragically assassinated on his way to an investor meeting [1]. This shocking event rattled investor confidence and coincided with soaring medical costs that began to swamp insurer profits [2].

As patients caught up on postponed care and doctors billed more aggressively (e.g., more tests per ER visit), UnitedHealth found its medical costs growing 20% year-over-year in Q2 2025 [3] – far above what it had priced into premiums. Expensive new drugs (for cancer, obesity, gene therapies) further strained costs [4].

By spring 2025, UnitedHealth had missed earnings estimates two quarters in a row and even took the rare step of cutting its full-year forecast in April, triggering a one-day $130 stock drop (its worst in 25+ years) [5].

In May, CEO Andrew Witty abruptly resigned amid these stumbles and forecast withdrawals [6]. Longtime former CEO Stephen Hemsley returned to stabilize the ship. When Q2 results came in weak, UnitedHealth slashed its 2025 earnings outlook to at least $16.00 per share – barely half its original ~$30 EPS target for 2025 [7]. (For context, analysts had been expecting ~$20.6 EPS, so even the reset outlook was below consensus [7].) The stock sank as low as ~$270 on this news, down ~55% from its peak and making UnitedHealth the worst performer in the Dow Jones index for 2025 [8].

On top of financial disappointments, UnitedHealth suffered a “laundry list” of bad headlines that hurt sentiment [9]. A massive cyberattack on its technology unit (the former Change Healthcare) in 2024 exposed the data of 192.7 million people – the largest healthcare data breach in U.S. history [10], causing system disruptions and reputational damage. The company also disclosed it is cooperating with federal investigators in an expansive fraud probe of its Medicare plans [11].

All these issues compounded to make UnitedHealth seem “untouchable” to many investors [12], and the entire managed-care sector became “beaten up and out of favor” in 2025 [13].

Subscribe now

However, August 2025 brought a spark of optimism: Warren Buffett’s Berkshire Hathaway revealed a new ~$1.6 billion stake (5 million shares) in UNH [14]. Other savvy investors like David Tepper’s Appaloosa and Lone Pine also bought in [15]. This “vote of confidence” sent UNH stock surging ~14% in one day [14]. Buffett is known for investing in quality companies during their darkest times, and his bet provided “psychological reassurance” that UnitedHealth’s long-term value remains intact despite its turmoil [12][14]. The stock rebounded to about $310 on the news. Still, analysts caution that turnaround will take time – the next 12–18 months are expected to remain challenging as UnitedHealth works through elevated costs and regains investor trust [13].

UnitedHealth’s Economic Moat and Competitive Position

Despite recent stumbles, UnitedHealth retains a formidable economic moat. It is the largest health insurer in the U.S. – its UnitedHealthcare unit serves ~51 million people and includes over 8 million seniors in Medicare Advantage, making UNH the #1 MA provider [16].

Moreover, UnitedHealth is vertically integrated through its Optum division, which encompasses:

Optum Health – clinics, surgery centers, and care delivery services.

Optum Rx – a top-tier pharmacy benefit manager (PBM).

Optum Insight – health data analytics and technology services (boosted by the 2022 acquisition of Change Healthcare).

This combination of insurance + PBM + provider + analytics creates synergies and high switching costs [17]. UnitedHealth can leverage data across the continuum of care, coordinate patient services, and manage costs in ways stand-alone insurers cannot.

Major competitors include Humana (MA-heavy), Elevance (Blue Cross), CVS (Aetna + Caremark), Cigna (Express Scripts), and Centene (Medicaid).

UnitedHealth’s market share and diversified services generally give it a wide moat – for example, it took in over $400 billion revenue in 2024 (Fortune #5), nearly double the next-largest health insurer [18].

Share

Legal Issues and PR Crises – Impact and Outcomes

UnitedHealth currently faces an overhang from a high-profile federal investigation into its Medicare Advantage practices. In mid-2025 the company disclosed it is cooperating with DOJ investigators examining whether it improperly inflated patient diagnoses to collect higher payments for Medicare Advantage plans [11].

Potential outcomes: If wrongdoing is found, UnitedHealth could face significant fines or settlements. For perspective, Cigna recently paid about $170 million to resolve similar allegations [19], and other insurers have paid tens of millions. For a company of UNH’s size, a fine in the low hundreds of millions would be a manageable one-time cost. The bigger risk is if reforms or oversight reduce the future profitability of Medicare Advantage. Regulators have signaled bipartisan concern about MA overpayments [20].

Aside from legal matters, UnitedHealth has been navigating unusual PR crises. The murder of Brian Thompson (the UnitedHealthcare division CEO) in late 2024 was a shocking event outside the company’s control [1]. With veteran Stephen Hemsley stepping in as CEO, leadership continuity is strong.

The cybersecurity breach at Optum/Change Healthcare, however, highlights a risk of financial and legal fallout. A breach affecting ~192 million people [10] could bring class-action lawsuits or regulatory fines. UnitedHealth will likely incur additional expenses for remediation, but historically (e.g., Equifax 2017) such breaches, while costly, were not franchise-ending [21].

Historical Analogies: Crisis and Recovery

Chipotle (CMG) – food safety outbreaks in 2015 halved its stock; by 2019–2020 it surpassed pre-crisis highs [22].

Equifax (EFX) – 2017 breach, stock down >30%, fully recovered in ~2 years [21].

Boeing (BA) – 737 MAX crashes; shares remain depressed years later [23].

Wells Fargo (WFC) – 2016 fake accounts scandal; stock never reclaimed pre-crisis highs, showing governance issues can cause permanent scars [24].

UnitedHealth’s troubles resemble Chipotle/Equifax more than Boeing/Wells Fargo: serious but fixable, not existential.

Outlook: Recovery Scenarios in the Next 6–18 Months

Looking ahead, the base case is a gradual recovery:

Base case: UNH trades back into the $350–$400 range by late 2026, assuming execution improves and costs normalize [25].

Upside: If medical cost pressures ease and DOJ probe ends lightly, UNH could approach $450 by 2026.

Full recovery ($500–$600): Requires multiple years, EPS near $25–30, and premium multiples restored [25].

Downside: Continued cost surprises or harsh DOJ actions could keep shares in the $270–$300 range.

Consensus analyst targets average $368 (range $198–$700) [25]. Buffett’s involvement suggests confidence in long-term rebound, but patience is required.

Conclusion

UnitedHealth’s moat and fundamentals remain strong. Its issues are serious but not permanent. Recovery to $350–$400 in 6–18 months is realistic; $500+ requires patience. The Buffett stake signals long-term value, but execution and cost control must prove it out.

References

[1] Reuters – CEO Brian Thompson assassination (2024)[2] Associated Press – Rising medical costs strain insurers (2025)[3] Reuters – 20% jump in patient medical costs Q2 2025[4] AP – Expensive drugs add to insurer cost burdens (2025)[5] Reuters – UNH earnings misses and forecast cut (2025)[6] Reuters/AP – CEO Andrew Witty resignation (2025)[7] Reuters – UNH EPS guidance slashed to $16, analyst reaction (2025)[8] Reuters – UNH worst performer in Dow Jones, stock at $270 (2025)[9] Reuters – “Laundry list of bad headlines” commentary (2025)[10] Associated Press – Optum/Change Healthcare breach, 192.7M records (2024)[11] Reuters – DOJ Medicare Advantage fraud investigation (2025)[12] Reuters – UNH seen as “untouchable” by some investors (2025)[13] Reuters – Managed care sector “beaten up and out of favor” (2025)[14] Reuters – Berkshire Hathaway discloses $1.6B UNH stake (2025)[15] Reuters – Tepper, Lone Pine also buy UNH (2025)[16] Reuters – UNH market share and Medicare Advantage leadership (2025)[17] Morningstar/Reuters – UNH vertical integration via Optum (2024)[18] Fortune – UNH revenue, scale vs peers (2024)[19] DOJ – Cigna $170M Medicare upcoding settlement (2023)[20] Reuters – Bipartisan scrutiny of Medicare Advantage (2025)[21] Reuters/MarketWatch – Equifax recovery post-breach (2017–2019)[22] Bloomberg – Chipotle post-2015 recovery (2019–2020)[23] Reuters – Boeing 737 MAX crisis impact (2019–2023)[24] Reuters – Wells Fargo fake accounts scandal fallout (2016–2023)[25] Reuters/Analyst consensus targets for UNH ($368 avg, $198–$700 range)

What do you think? Do you buy CGPT’s assessment?

Is it more like Chipotle than Boeing?

What else?

Leave a comment

Share